THE BOUNCED CHECK RACKET A Look at Predatory Banking Practices

by James Jaeger

Intro and Update:Since this article was written on 15 March 2003, Citizens Bank was sued at class action and agreed to pay $137.5 million to settle. Read the Bloomberg article here or below.(0)

Embarrasment Most of us have a checking account. Accordingly, most of us have, at one time or another, inadvertently bounced a check -- even Congressmen have managed to do this, but few talk about it -- or at least they suppress the subject for as long as possible, as in the case of the Congressmen until their check-bouncing scandal went public. Indeed, this is a subject everyone likes to sweep under the carpet because no one wants to "look poor," or worse, be guilty of passing a "rubber check." But did you know the banks actually WANT you to pass "rubber checks" because this is a little multi-billion dollar revenue stream for them, a racket they have engineered and fine-tuned with computer-precision over the years?

The problem is the barrage of "insufficient funds," "unavailable funds" and "uncollected funds" charges that are levied on customers' accounts are not only excessive and confusing, they run counter to the best interests of society. After studying the Federal Reserve member banks' arcane, predatory policies; new, confusing balance terminology; and non-standard fiscal days, I would like to shed some light on a business practice which needs to be voluntarily changed by the banks, or addressed by class action and government regulation. Inevitably the later will be the only remedy because, like the vicious tobacco companies, too much money is at stake.

Let me start by saying this: this article is not meant to target or invalidate any of the many good services banks provide, or to denigrate ethical bankers, several of whom I have had the pleasure of working with in the past, including one, a manager, who confirms what you are about to read.

Clearly, not all banks have mercenary or predatory policies, but the ones that do -- the ones that are taking advantage of the public, especially the elderly, poor and young depositors -- need to be addressed(1).

The Mechanics of Insufficient Funds Charges When a bank customer writes a check on an account in which there are insufficient funds to cover the check (or uncollected funds deposited but not yet counted in the balance), the bank either RETURNS the check (known as a "bounce") or PAYS the check and then charges the customer's account a fee of as much as $31. This fee is usually called a "nonsufficient funds fee" or an "insufficient funds fee" and is levied on the customer's account within a matter of hours by internal electronic transfer, customer-to-bank. Usually this fee is charged instantly by computer algorithms set up to debit any account in the event certain parameters develop. Often this happens AFTER banking hours or late at night, and with increased frequency in the late or wee hours between Tuesday and Wednesday morning. These particulars, of course, vary from bank to bank and state to state.

Many times the customer is TOTALLY INNOCENT, yet gets charged by this robotic, computer-driven system regardless. For instance, if someone gives you a check that is "bad" (i.e., a check not covered by funds in their account), and you deposit it and write new checks against it on faith that their check is "good," all the new checks you write will "bounce." In this case, you are innocent, yet you will get charged as much as $31 for each bounce -- and the banks will profit from your misfortune.

Even though the law requires the bank to "immediately" give notice to the customer that his check has "bounced," it does NOT require that the bank must debit the customer's account a nonsufficient funds fee at the time the deficiency shows up or notice is given. The fee can be debited at any time and this is "arbitrarily" left up to the bank's policy board. But, as you will see below, by fine-tuning this socially repugnant business practice, the Federal Reserve-member banks -- most probably your bank -- generates enormous profits at your expense and, in all likelihood, because of your reluctance to complain due to the embarrassment discussed above.

In more detail, here is the chain of events that happens to millions of people every day across the world, and has probably happened to you at one time or another:

- When the bank charges a nonsufficient funds fee, this charge immediately reduces the balance in your account. This may cause other checks in your account to bounce, especially if: a) your balance is low, b) the check that made your account overdrawn ("Offending Check") is paid by the bank, or c) the Offending Check amount is higher than other checks that might be outstanding in your account. Even a check for $1 will now bounce because the bank has instructed its computers to debit your account (in the middle of the night) a fee for as much as $31 for each Offending Check. If you have many small-denomination checks outstanding, these will ALL also bounce. Then, each of these new bounces -- bounces that could be said to be caused by the bank at this point -- incur additional $31 charges against your account, draining further funds or placing it in debt (i.e., overdrawn status). Often the he banks debit the largest checks first. They do this so they can create the highest probability that the greatest number of smaller checks will bounce. Each bounce means $31 revenue for them and a $31 charge against your account. The more charges there are against your account, the greater still the probability that MORE checks will bounce. This banking practice sets up what's known in science as a "negative feedback loop." Such negative feedback loop sets up a vicious cycle which can easily cost you fees of $62, $93, $155 or $310 before you even receive notice in the mail that there is a problem with your account! And this is, of course, the banks' intention and the source of an enormous profit center.

- It's not long before you are feeling confused, helpless and even totally outraged because, at this point, you are often unable to render a normal bookkeeping or interim reconciliation of your account to get things back on track (or even figure out what happened and who is at fault).

- You are then forced to contact your bank service representative (after wading through their impersonal voicemail system) to find out what's happening, how many checks have bounced, what the bank has been debiting from your account in the middle of the night, what the current balance is and, again, WHY it all went off the rails in the first place. The bank service representative must now take time to discuss the account with you (or hang up on you because you're now screaming) and you must get in your car and DRIVE to your bank. Because the bank service representative is a paid (sometimes minimum-wage) employee, all this is also an expense to the bank -- an expense for a situation that should never have been started in the first place, by either you or the bank. The upshot of the often-nasty conversation with the bank service rep is usually that they don't know what the state of affairs of the account is because they have no idea what checks you have issued or which ones have been deposited. By the same token, you may not know which checks the bank has bounced because the notices have not been generated yet or the charges have not showed up on the bank's computer yet. Often you will get some cocky young kid who is determined to "help" you figure out why it was all your fault. He's computerized and can pull up all your records on past bounced checks, especially the situations where it was YOUR fault, not the bank's. The other situations, where it was "bank error," as they term it, are often conveniently not on record.(2)

- Thus, the only stop-gap "remedy" for the escalating situation is for you to rush out and get a bunch of cash and deposit it into your account immediately. This "forced-deposit" necessitates drawing money from another account, liquidating an asset, raiding the mattress, borrowing from a hostile (but possibly richer) family member/friend, kiting, or just saying to hell with the account and letting it go down the tubes. If you choose the latter, you will suffer the bullet of one more debt, and a blot on one of the many bank-serving, credit-reporting agencies (such as TRW, Trans Union or Equifax) that are always circling like vultures(3). What's worse, you may be placed on the bank's "fraud list" and, as a result of being on this list, you will be unable to open another checking account anywhere with a Federal Reserve-member bank. Thus the banking cartel has you trapped like a rat in its fiat maze. Accordingly, your ability to operate in "modern" economic society is thus truncated to that of cash 'n carry and money orders. Not a bad way to go, but you're still considered a second class citizen by the banking elite.

The sum of $62 (an insufficient funds fee charged from just two bounced checks) can mean a week of food money for someone who is unemployed, a senior citizen on a fixed-income, or a youngster just out of college who is still becoming familiar with the financial planning required in day-to-day life. Such people, especially the elder, often have difficulty keeping, or reconciling, a check register under normal conditions -- let alone under the conditions generated in the nightmare of insufficient funds inflicted by banks.The upshot of the above economic litany is that the CUSTOMER and the BANK are involved in extensive amounts of time to reconcile the account (and argue) -- time which can easily amount to hours over the course of a day or more. The customer usually has to take time off work (as banks are only open for a small window of time each workday) and undertake extraordinary measures to remedy the situation, all of which cuts into his or her responsibilities, both familial and job-related. THIS CAUSES DAMAGE TO SOCIETY BECAUSE IT FORCES PEOPLE TO WITHDRAW ATTENTION FROM THEIR PRODUCTIVITY AND PLACE IT ON BANK-GENERATED NONSENSE. It preempts people's time to handle a situation that is self-serving and profitable for the banks. Any way you slice it, this system is a terrible inconvenience, if not an unscrupulous racket for the Federal Reserve-member banks. When you consider that this racket is being imposed on millions, if not tens of millions, of people all over the U.S. and world on any given day, imagine what the forced-deposits (see step 4 above) and automatic-fees represent in monetary terms to the banks?

One of my bankers, an honest man from India (who shall remain unnamed, lest he be fired), told me in absolute terms the following: "The banks exploit the NSF profit center knowingly and with a high degree of precision. For them, it amounts to a profit of about $18 billion per year and it's without question at the customer's expense. Either the banks get money out of you from the bounced checks or they force you to borrow with overdraft protection. What they are doing is basically what the mob does, selling protection from themselves."

Again, this system is not only antisocial -- because the customer loses time and money -- but the customer's business connections lose time and money, the business world loses time and money and, in the end, the society loses over the waste of human resources.

The worst thing is that the "Bounced-check System" has been engineered by bank managements and owners to be a covert profit center. Unfortunately this profit center exploits basically honest people, many of whom are just trying to survive or who, again, are often too embarrassed to admit that they have "bounced a check" (as a bounced check is often taken as a symbol of being either low on money or financially irresponsible). Thus, few raise the issue and the banks continue exploiting people and society with their nefarious little profit scheme. This is but one scheme among many reported in a book entitled The Creature From Jekyll Island by G. Edward Griffin.

Case-in-Point When the bank debits an insufficient funds fee from a customer's account, it is usually 2 to 4 days before the customer becomes aware (by mail) that $31 has been debited from his or her account.

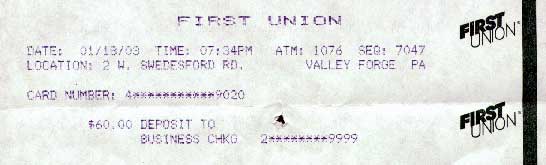

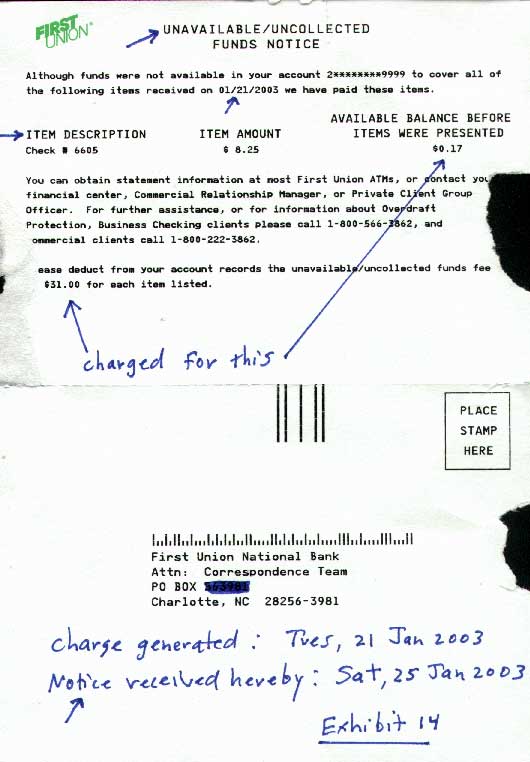

Here's a real-life occurrence where a customer's account had, according to the BANK, $0.17 (17 cents) in it on January 21, 2003 even though the sum of $60.00 cash had been deposited to the account in a MAC machine right on the BANK's premises on January 18, 2003. (See deposit receipt here)

On January 21, check #6605 for the sum of $8.25 was presented to the BANK for payment. Even though the BANK had in its possession the sum of at least $60.17 cash, they considered the $60.00 as "unavailable or uncollected funds" and thus charged this account a fee of $31.00. All this happened between Tuesday and Wednesday morning (January 21 and 22, 2003). However, the UNAVAILABLE/UNCOLLECTED FUNDS NOTICE, having been mailed, was not even received by the customer until Saturday, January 25, 2003 -- and the only reason it was not received later was because the customer just happened to be in the office on Saturday, otherwise it would not have been received until Monday, January 27, 2003 -- 6 days later!

Thus, what in essence is happening here is the BANK is charging the sum of $31.00 to a customer for paying an $8.25 check even though they have at least $60.00 of the customer's cash on hold from Monday the 18th of January, THRU Monday, the 20th of January (a holiday) and into Tuesday the 21st of January. The BANK'S computers and policy seem to be QUICK to debit and SLOW to credit. Thus increased fees are generated at the expense of the customer.

Letter to My Bank Here's another case-in-point. The below letter is purportedly an actual letter that was sent to a bank by a 96-year-old woman. The bank manager thought it "amusing" enough to have it published in the New York Times.

Dear Sir:This letter would be funny if this predatory banking system were not so serious. It's interesting to note that, if it actually WAS a bank manager that sent this letter to the New York Times, a premise I seriously doubt, it's pathetic that such manager did so to ostensibly make light of the situation: a racket that victimizes mostly the poor, the young, and in this case, as mentioned above, the elderly.I am writing to thank you for bouncing my check with which I endeavored to pay my plumber last month. By my calculations, three nanoseconds must have elapsed between his presenting the check and the arrival in my account of the funds needed to honor it. I refer, of course, to the automatic monthly deposit of my entire salary, an arrangement which, I admit, has been in place for only eight years.

You are to be commended for seizing that brief window of opportunity, and also for debiting my account $30 by way of penalty for the inconvenience caused to your bank. My thankfulness springs from the manner in which this incident has caused me to rethink my errant financial ways. I noticed that whereas I personally attend to your telephone calls and letters, when I try to contact you, I am confronted by the impersonal, overcharging, pre-recorded, faceless entity which your bank has become.

From now on, I, like you, choose only to deal with a flesh-and-blood person. My mortgage and loan repayments will therefore and hereafter no longer be automatic, but will arrive at your bank, by check, addressed personally and confidentially to an employee at your bank whom you must nominate.

Be aware that it is an offense under the Postal Act for any other person to open such an envelope. Please find attached an Application Contact Status which I require your chosen employee to complete. I am sorry it runs to eight pages, but in order that I know as much about him or her as your bank knows about me, there is no alternative. Please note that all copies of his or her medical history must be countersigned by a Notary Public, and the mandatory details of his/her financial situation (income, debts, assets and liabilities) must be accompanied by documented proof.

In due course, I will issue your employee with a PIN number which he/she must quote in dealings with me. I regret that it cannot be shorter than 28 digits but, again, I have modeled it on the number of button presses required of me to access my account balance on your phone bank service. As they say, imitation is the sincerest form of flattery.

Let me level the playing field even further. When you call me, press buttons as follows: 1. To make an appointment to see me. 2. To query a missing payment. 3. To transfer the call to my living room in case I am there. 4. To transfer the call to my bedroom in case I am sleeping. 5. To transfer the call to my toilet in case am attending to nature. 6. To transfer the call to my mobile phone if I am not at home. 7. To leave a message on my computer, a password to access my computer is required. Password will be communicated to you at a later date to the Authorized Contact. 8 To return to the main menu and to listen to options 1 through 7. 9. To make a general complaint or inquiry.

The contact will then be put on hold, pending the attention of my automated answering service. While this may, on occasion, involve a lengthy wait, uplifting music will play for the duration of the call. Regrettably, but again following your example, I must also levy an establishment fee to cover the setting up of this new arrangement.

May I wish you a happy, if ever so slightly less prosperous New Year?

Your Humble Client

A Third Case-in-Point Here's a report of what happened to Debbie Hagan of Owensboro, Kentucky

I normally don't look at my snail mail statements but once every three months. But when all of a sudden, after making plenty of deposits last month, my ATM card was declined, I was surprised and went online to look at my balance. I was over $700 OD!! Mouth fell open! Then I got to really looking, and looking close. Of course the paper statements are confusing to really analyze . . . deposits grouped together, checks grouped together, ATM/Debit grouped in another area. Makes it difficult to follow the process of things. The online statement is a bit clearer, HOWEVER, it makes it look like the process from low to high, so when you look at the stuff on the next day you don't understand all the different OD fees! This is just disgusting, is all I can say.I went back as far as April (just assuming the balance was correct then, which I'm sure it wasn't) and from April until October 14 I should have about 2K in the bank, but instead I have -$1200 or so. (Hard to keep up with, since I get charged $6 per day just because.) That's when I go online (so thankful for Internet) and starting researching and found how lower income or people who keep balances in bank low, are being deceived, abused and basically shit upon. Boy, did my blood start to boil. Then I found the websites of these companies who designed these programs to assist the banks in the fraud, and read the "testimonials" from bankers on how their fee income had increased and I got on a bandwagon, big time.

The effect is hard to measure that this has. There are no telling how many bills I would have been able to pay (on time) if the money was there for my use, as it should have been. So then you get into late fees. If you are close to being maxed on your CC, they can through you over limit, then you get into another whole set of fees. It's hard to be poor, or live paycheck to paycheck.

I could use all the information and advice I can get. This is not personal anymore, not to me anyway. It's about getting something done, making a change and helping those like me who have been duped.

Check 21 My Balance In order to "facilitate" the collection of "insufficient funds," "unavailable funds" and "uncollected funds" fees, the banks have now gotten Congress to pass "CHECK 21" legislation. Check 21 stands for "check clearing for the 21st Century." The new system is designed to allow the banks to use digital copies of your check rather than the original. This means your proof of payment is now transferring from your hands to the bank's hands as they will have the authority to destroy your checks even before they have settled.

The American Banking Association and the Federal Reserve-member banks are positioning this system as a new quicker way to process checks by allowing the banks to wire-transfer (Internet-transfer) digital images of checks rather than having to truck the original paper versions from bank to bank for settlement. This all sounds good except for one thing: It has the potential to remove the "float," thus causing more bounces and further frustrating commerce. The "float" is the interval of time between the time someone writes a check and the time that check is cashed, creating a balance. But have you called your bank for a BALANCE lately? If your bank is like WACHOVIA, you will get two "balances" for a personal account and three "balances" for a business account. These balances are as follows: LEGDER BALANCE, AVAILABLE BALANCE and COLLECTED BALANCE. All three of these numbers can, and usually ARE different. Gone are the days when your balance is your balance. Confused? You're supposed to be. But in case you're not, check out what the actual definitions of these so-called balances are, according to the banks:

Clear now? Sure, if you are an accounting major or have a CPA. But that's the exact point: The less certain the general public is as to what their EXACT balance is, the greater the probability they will OVERDRAW, thus giving the bank a "justification" to charge another $31 bounced check charge. The banks will, of course, claim that they are just trying to be more specific, that they are trying to more accurately differentiate the flows of money in and out of your account. But rest assured, when were the banks your buddies? Combine BALANCE OBFUSCATION with zero float, due to CHECK 21, and you have a recipe for extorting more "insufficient funds fees," "unavailable funds fees" and "uncollected funds fees." Little old ladies, teenagers and people on the minimum wage -- beware. Since the ultimate goal of CHECK 21 is to provide greater liquidity to M2, it will be interesting to see if the public actually benefits from this, and if banks actually use the CHECK 21 system to CREDIT accounts as quickly as they DEBIT them. If a bank can DEBIT all the payable checks from your account BEFORE they CREDIT your deposits, guess what -- you get bounces, hence $31 charges. In my personal banking, I have, on occasion, noted that banks will DEBIT checks from my account BEFORE they CREDIT them. This is especially true when one is making deposits in ATMs or after the fiscal banking day ends, usually at 3 pm. The bank managers tell me that all DEPOSITS are credited BEFORE checks are charged against the account (debits), but it is simply not true. Along with the game of debiting the largest denomination checks first to drive the balance down, the practice of debiting items before crediting items is a wonderful game that is a real revenue generator for the Federal Reserve-member banks.

- "Your LEDGER BALANCE is the balance after all deposits have been posted at the end of the last business day."

- "Your AVAILABLE BALANCE is your ledger balance plus or minus any intra-day adjustments, such as wire transfers and debit transactions."

- "Your COLLECTED BALANCE is your ledger balance minus FLOAT."

- "The FLOAT is the current amount of outstanding items in the process of being collected from other financial institutions."

All in all, it's still too early to see what actual effect CHECK 21 will have on commerce, but, again, my guess is that it will cause MORE checks to bounce, and hence generate MORE revenue for the banks. Given the element of confusion over BALANCES, the ability to now INSTANTLY transfer money OUT of your account and the bank's ability to HOLD or DESTROY the originals of your checks, even in the event of a problem, I bet you will see an enormous revenue peak for the banksters as well as an optimization of their positions in litigation.

People get the kind of banking system they deserve . . . especially when they are asleep during the legislation that is passed -- legislation, I might add, that you hardly EVER hear the Corporate Media informing you of until AFTER the fact. By removing the float from society, the banks are, in essence, removing the oil from the wheels of commerce. People live busy lives. They can't always make deposits and do their banking on cue or with brutal computer accuracy. My call is: CHECK 21 will, in the end, remove the float from the hands of the People and place it in the hands of the Banks, who will profit from it further. Time will tell.

A Possible Solution First of all, banks should not pay checks when there are insufficient funds in an account, thus the bank would be protected from any loss of that nature.

Secondly, insufficient funds charges should not be levied until after the customer has had reasonable time to have received notice. Alternately, they should be assessed when the customer's monthly statement is cut, along with all other service charges -- not in the middle of the night between Tuesday and Wednesday by computer drones.

The bank that is charging a standard service or activity fee for managing the customer's account is in essence "double dipping" when it also charges a $31 fee to administer the handling of insufficient fund situations because this fee is excessive in light of the service rendered and the bank does not state that this fee is punitive.

The fact that the bank debits a $31 fee from a customer's account before the customer even knows about the debit indicates that the bank assumes its accounting is correct and the customer's accounting is in error. The agreement between the bank and the customer cannot absolve the bank for its errors or policies contrary to law or public opinion, especially when the bank is acting in a fiduciary capacity. Accordingly, customers cannot waive their rights, and the bank cannot expect that a right is waived by placing a deposit agreement between the bank and the customer that is fundamentally fraudulent, usurious or against public policy.

If the bank's accounting turns out to be in error and the customer's accounting correct, it could be construed that the bank has in effect embezzled money from the customer because of the following: There is an employee, agency or fiduciary relationship between the bank and the customer; the customer's money came into possession of the bank by virtue of that relationship and the customer's money was intentionally and fraudulently appropriated by the bank, causing damages (as delineated above).

The reason I say "fraudulently appropriated" is because one of the strongest elements of fraud is the intention to deceive. Because of various ABA meetings that are public record, it is evident that senior management of banks is well aware of this bounced check fee practice and has expressly intended for it to be a profit center. In fact, at least one bank, if not many or all, has acted to bolster its profits by such despicable practices as processing larger-denomination checks first to increase the likelihood that greater quantities of smaller-denomination checks will bounce.

The fact that the customer's account is thrown into accounting uncertainty by fee withdrawals (unauthorized by the customer in real time), places the bank at an advantage and the customer at a disadvantage such that the customer can easily be deceived by the bank (knowingly or unknowingly) as to the status of his or her balance. This set of circumstances thus brings about a financial gain for the bank and a financial loss for the customer. Many customers pay the excessive bounce fee(s) in ignorance or under duress. This occurs when they assume the bank, due to its institutional status and/or superior computerized bookkeeping system, will usually be correct when in fact they are in error, or the element of embarrassment causes duress, so they just pay up and shut up. Under such circumstances the contractual relationship between the bank and the depositor takes on the nature of a contract of adhesion.

Banks should take a serious look at their policies as they relate to the handling of insufficient funds and if what I have discussed here makes sense to them on a broader social level, or if it can improve customer relations, they should change this negative feedback loop as soon as possible.

Unfortunately, in all probability, banks will not change their policies because of the significant sums they are making. This situation is similar, albeit on a smaller scale, to the tobacco companies when they refused to respond to public concern about their exploitive activities. As evidence of this claim, around 1995, I sent a letter to Eugene Ludwig, then Controller of the U.S. Currency, outlining the above points. At that time, insufficient funds fees were generally about $20, as opposed to the $31 (and higher) that many banks were charging as of 2003. Not only did I receive zero response from Mr. Ludwig, but it appears that the situation has become worse. Not only are more excessive fees being charged for "insufficient funds," but now the banks have added a new way of "justifying" such fees: They have added the game of "unavailable funds" and "uncollected funds" to their arsenal of tricks. This means that they are able to not only charge you a $31 "insufficient funds" fee if your account is OVERDRAWN, but they can charge you an "unavailable funds" or "uncollected funds" fee if your account only has UNCOLLECTED funds -- meaning funds that have not yet been credited to your account through the banking system, an action that is entirely out of your control as the customer.

Thus the only remedy for this situation will probably be class action law suits and new government regulations. Surely, there are millions of people who, at one time or another, have been victimized and outraged by this system but have never mentioned it to anyone. Until this negative banking practice is removed from society, perhaps the only thing one can do is remove their money from Federal Reserve-member banks and place it in credit unions with more reasonable policies.

Copyright 2004 by James R. Jaeger II The copyrightholder of this document hereby grants a general license to any NATURAL PERSON to use all or part of same IN CONSIDERATION FOR: a) your forwarding it to at least three (3) other natural persons OR b) your reporting to the copyrightholder any errors or comments on the contents hereof.

----------------------------

(0) (Bloomberg) "Citizens Bank agreed to pay $137.5 million to settle a class-action lawsuit accusing the bank of manipulating customers� debit card and ATM transactions in order to generate excess overdraft fees. The lawsuit is part of multidistrict litigation involving more than 30 different banks before US District Judge James Lawrence King in Miami, lawyers at the law firm Grossman Roth said in a statement announcing the settlement. Plaintiffs� lawyer Robert C. Gilbert expects the settlement to be presented to the court for approval later this year, according to the statement. Citizens Bank was accused of using software programs to re- sequence debit card and ATM transactions by posting them in highest-to-lowest dollar amounts, rather than in the order in which the transactions occurred, to increase the number of overdraft fees, according to the statement. Citizens Bank is a unit of Citizens Financial Group Inc., the US consumer and commercial lender Royal Bank of Scotland Group Plc bought in 1998. Jim Hughes, a Citizens Bank spokesman, said in an e-mailed statement the bank is pleased to �have this matter behind us.� The case is In re Checking Account Overdraft Litigation, 09-md-02036, US District Court, Southern District of Florida (Miami)." Source: http://www.boston.com/Boston/businessupdates/2012/04/citizens-bank-pay-million-settle-overdraft-suit/TqQwQbhhvsg4Xw3VOIFNcM/index.html?p1=News_links(1) This discussion does not address the Federal Reserve System in general, as discussed in such books as The Creature From Jekyll Island by G. Edward Griffin (a complete review of the book available at http://st3.yahoo.com/realityzone/creature2.html#review).

(2) Often the bank service representative will reverse a certain amount of "bounced check" charges or "negotiate" with the customer as to what portion of them can be reversed. This is a nice gesture, but often to arrive at this point, much time is absorbed by both the representative and the customer. In the end, the customer still ends up paying an excessive fee because the fees are excessive to begin with.

(3) The credit card reporting agencies actually serve the banks under the guise of serving the public. Since most of the money the Federal Reserve bank issues is generated out of thin air from monetizing debt or fractional reserve, the banks lose little or nothing when a depositor defaults. (See http://www.jaegerresearchinstitute.org/articles/money.htm for more information). Thus the credit card reporting agents are protecting nothing. What they ARE protecting is profits. They do this by creating a financial dossier on you (similar to, but not as extensive as the dossiers that were used in Nazi Germany) so that the banks are in a better position to use this information to extort higher interests rates and points out of you. To the degree the banks have adverse "credit reports" at their disposal, their sales force (known as "loan officers") has the "justification" to charge you higher rates and points for your home mortgage and consumer credit. The loan officers explain that these higher fees are needed "because they are taking more risk" on lending you the money they have created out of nothing.

(4) TESTIMONIALS:

Hello. I have been fit to be tied over the problems I have had with my bank over bounced checks. I have gone round and round with National City Bank for the past 6 years regarding their practices and just don't know what to do.

They have collected probably thousands of dollars from me over the past 6 years as a result of their unscrupulous practices. National City has consistently and every time they found the opportunity, paid the largest items that come in on my account first, which leaves all the small ones to bounce, despite the fact that there would have been plenty of money to cover the small items. Due to the fact that they charge me a $34 to $36 fee (I haven't figured out yet why that changes regularly) for each NSF or OD, I have incurred probably three times the amount of overdraft fees that I should have incurred, if not more.

When I contact the bank regarding incidents, I am told that my "overdraft history" precludes them from being able to show me any mercy. My extensive "overdraft history" is a direct result of their practice of paying items largest to smallest and they have admitted to me that they do this. I have requested in the past that this not be done, but they have not heeded this request. I recently sent a written request directing how I want the monies paid from my account. I am waiting for a written explanation of why they will not be able to honor this request.

Most recently, I discovered today that I was charged two $34 overdraft fees because of an automatic transfer of $25 from my checking to my savings, which occurs once monthly. Despite the fact that I had only $14.96 in my account, the bank transferred $25 to my savings account, and then debited my account $34 for this favor. They then paid my $4.31 debit charge and charged me $34 for that. I still have a $10 check out which will be coming in, and for which I will be charged another $34 because I am literally flat broke until payday at the end of the week.

Mind you, I had sufficient funds to cover the $4.31 and the $10 debit. I was trying very hard to be responsible and I check my balance online nearly every day. The bank suggested to me that I sign up for this $25 transfer service because it was supposed to be a positive service. No one ever told me that they would take $25 out of my account even if I didn't have it to transfer to MY OWN savings account. When I had NO money in my account, they did not place $25 in my savings and then charge me an NSF charge for this, despite the fact that there was an order on my account at that time to transfer $25 to my savings.

I went round and round with the bank about this and literally got nowhere. There have been several other situations where things occurred that were not my fault, but the fault of a merchant, etc., and the bank refused to reverse the charges. To be fair, there have been a few times when charges were reversed, but that probably amounts to about 5% of the time, I would say.

I am very interested in a class action lawsuit. Do you know if anyone has taken any action concerning this matter or if anything is in the works?

I can be reached at barrerat@michigan.gov or at mercyrainz@sbcglobal.net.

Thank you,

Tawnne A. Barrera

ORIGINATED:15 March 2003

UPDATED: 25 APRIL 2012

Please forward this to your mailing list. The mainstream media will probably not address this subject because they have conflicts of interest with their advertisers, stockholders and the political candidates they send campaign contributions to. It's thus up to responsible citizens like you to disseminate important issues so that a healthy public discourse can be initiated or continued. Your comments and suggestions are welcome and future versions of this research paper will reflect them. Permission is hereby granted to excerpt and publish all or part of this article provided nothing is taken out of context. Please give reference to the source URL.

Any responses you proffer in connection with this research paper when emailed or posted as an article or otherwise, may be mass-disseminated in order to continue a public discourse. Unless you are okay with this, please do not respond to anything sent out. We will make every effort, however, to remove names, emails and personal data before disseminating anything you submit.

Don't forget to watch our documentary films listed below so you will have a better understanding of what we believe fuels most of the problems under study at Jaeger Research Institute. We appreciate you referring these documentary films to others, purchasing copies for your library, screening them for home audiences and displaying them on your public-access TV channels. The proceeds from such purchases go to the production of new documentaries. Thank you.

If you wish to be removed from this mailing list go to http://www.jaegerresearchinstitute.org/mission.htm but first please be certain you are not suffering from Spamaphobia as addressed at http://www.jaegerresearchinstitute.org/articles/spamaphobia.htm

SOURCE URL

http://www.JaegerResearchInstitute.org

| FIAT EMPIRE | ORIGINAL INTENT | CULTURAL MARXISM | CORPORATE FASCISM | SPOiLER |

Mission | Full-Spectrum News | Books & Movies by James Jaeger | Sponsor |

Jaeger Research Institute

{kind=link}

{kind=link}